Responding to the now weeks-long, trucker-led protests that have snarled streets in Ottawa and blocked key crossings at the U.S.-Canada border, Canadian Prime Minister Justin Trudeau this afternoon invoked the Emergencies Act for the first time since the law was passed in 1988.

“This is about keeping Canadians safe, protecting people’s jobs, and restoring faith in our institutions,” said the prime minister. Though the Emergencies Act allows for the military to be called in, Trudeau, for now, said he has no plans to do so.

The government instead appeared set to take aim at protesters’ finances. Speaking alongside Trudeau, Deputy Prime Minister Chrystia Freeland said banks can immediately freeze or suspend bank accounts without a court order and without fear of civil liability.

In addition, the government is broadening the scope of Canada’s anti-money laundering and counter-terrorist financing rules to now cover crowdfunding platforms and the payment service providers they use. These changes, said Freeland, cover all forms of transactions, including digital assets such as crypto.

The Tallycoin bitcoin fundraiser had reportedly raised more than 20 bitcoin (BTC) – or nearly $1 million – for the truckers. The organizers have shut down the fundraising page, and are asking everyone to “stay tuned” about the next steps.

ECB President Christine Lagarde talked about the digital euro at the plenary session of the European Parliament Monday on the 20th anniversary of the introduction of euro banknotes and coins.

“Last year, we launched the digital euro project,” she said. “We will investigate how a digital euro could offer a convenient, cost-free means of payment, allowing people to pay anywhere in the euro area with risk-free digital money – for example, when making payments online, which preclude the use of cash,” the ECB chief continued, emphasizing:

In any event, a digital euro would complement cash, not replace it. This is also why we launched the process for redesigning our banknotes.

The European Central Bank launched a two-year investigation into a digital euro in October last year. “Once the investigation phase has ended, we will decide whether or not to start developing a digital euro. We would then create and test possible solutions, working together with banks and companies which could provide the technology and the payment services,” the ECB clarified.

The ECB website details: “The digital euro would still be a euro: like banknotes but digital. It would be an electronic form of money issued by the Eurosystem (the ECB and national central banks) and accessible to all citizens and firms.” It adds:

A digital euro would give you an additional choice about how to pay and make it easier to do so, contributing to accessibility and inclusion.

Meanwhile, the European Commission is planning to put forward a bill to lay down the legal foundation for a digital euro. The legislation will support the ECB’s work on the digital euro. “Our goal is to table legislation in early 2023,” said Mairead McGuinness, European commissioner for Financial Stability, Financial Services, and the Capital Markets Union.

IMF Managing Director Kristalina Georgieva gave a speech last week at the Atlantic Council in Washington D.C. regarding the future of money, cryptocurrency, and central bank digital currencies (CBDCs).

Noting that central banks have moved beyond conceptual discussions regarding digital currencies and are in the experimentation phase, she noted: “These are still early days for CBDCs and we don’t quite know how far and how fast they will go.”

Nonetheless, the IMF chief said:

If CBDCs are designed prudently, they can potentially offer more resilience, more safety, greater availability, and lower costs than private forms of digital money.

She continued: “That is clearly the case when compared to unbacked crypto assets that are inherently volatile. And even the better managed and regulated stablecoins may not be quite a match against a stable and well‑designed central bank digital currency.”

The IMF boss said that around 100 countries are exploring central bank digital currencies.

She mentioned the Sand Dollar in the Bahamas, a proof-of-concept by Sweden’s Riksbank, and the e-CNY in China. In addition, she recognized that the U.S. Federal Reserve issued a report on CBDCs last month.

Georgieva revealed:

The IMF is deeply involved in this issue, including through providing technical assistance to many members. An important role for the Fund is to promote exchange of experience and support the interoperability of CBDCs.

She proceeded to share some of the lessons learned from various central banks from their digital currency efforts.

The largest bank in Switzerland, UBS, published its view on U.S. crypto legislation Friday after the House of Financial Services Committee held a lengthy hearing on the regulation of cryptocurrencies and stablecoins last week.

The Swiss bank’s U.S. Office of Public Policy explained that at the hearing, a senior Treasury official discussed recommendations made in a stablecoin report issued by the Department of the Treasury and other regulators.

“To fill in regulatory gaps and address financial stability concerns, the regulators would like Congress to develop legislation that regulates stablecoin issuers as banks,” the UBS team detailed, noting that this proposal has received pushback from some lawmakers.

The Federal Reserve also made it clear in its recent central bank digital currency (CBDC) report that it would like direction from Congress before proceeding with a digital dollar.

However, Switzerland’s largest bank believes:

It will take time for lawmakers to digest the complexities of these issues and reconcile potentially divergent approaches on how digital assets should be regulated.

The UBS team further detailed: “Regulators could be waiting a long time for Congressional action and in the meantime will need to grapple with these issues using the limited and imperfect authorities they already have.”

Nonetheless, the bank pointed out that interest in crypto assets “is growing in Congress and among the broader public.”

Furthermore, there are reports that the Biden administration may weigh in on cryptocurrency legislation with an executive order in the near future.

In August last year, U.S. Senator Ted Cruz slammed his colleagues in Congress for trying to regulate crypto without an understanding of what it is.

The senator from Texas said: “We shouldn’t regulate something we don’t yet understand. We should actually take the time to try to understand that. We should hold some hearings, we should consider the consequences … We shouldn’t destroy people’s lives and livelihoods from complete ignorance.”

Meanwhile, two federal agencies — the U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) — are collaborating to ensure investor protection in the crypto space.

Bitcoin held above the $41,500 resistance level over the weekend after a slide from the $46,000 level last week. The move came as hash rates for the Bitcoin network hit lifetime highs.

Bitcoin has shown strength this month after a slide to yearly lows of $33,000 in January. It broke above the $38,000 and $41,500 resistance level in the first week of February to monthly highs of $46,000, a level previously seen in the final weeks of 2021.

Traders have since taken profits on the move as bitcoin saw weekly lows of $41,600 in early Asian hours on Monday but recovered to nearly $42,000 in afternoon hours.

Bitcoin hit resistance at $45,000 and has since fell. (TradingView)

RSI, or Relative Strength Index, levels showed readings of 39 on Monday, suggesting an end to the weekend slide and a continuation of the uptrend to the $48,000 level.

RSI is a price-chart indicator that calculates the magnitude of price changes. Readings above 70 suggest an asset is “overbought” and could see a correction, while below 30 imply “oversold” wherein assets may recover.

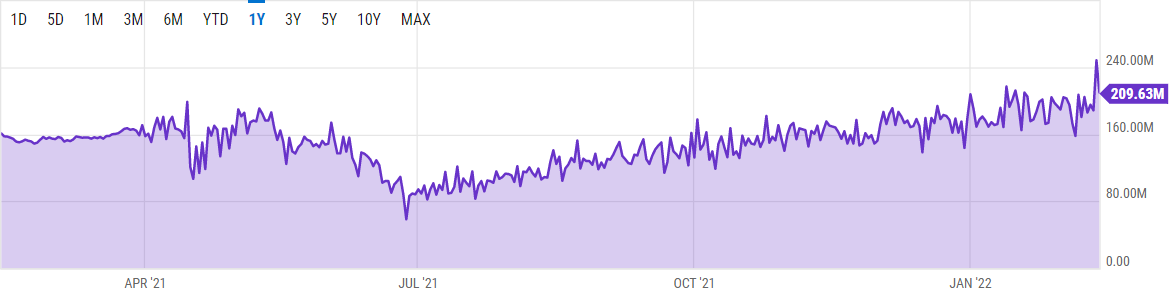

The weekend price action came as hashrates surged to new all-time highs, as per data from analytics tool YCharts. Hashrates are a measure of the computing power required to mine blocks on the Bitcoin network, and higher rates make it much more difficult for singular entities to try and control the network in the so-called “51% attack.”

Hashrates hit 248.11 million terahashes per second (TH/s) on Saturday, increasing from the 180 million TH/s level from last week. It currently hovers at 209.63 million TH/s, falling 15.51% in the past 24 hours, data show.

The Hash rate surged to all-time highs. (YCharts)

Bitcoin hashrates have increased by over 50% in the past year. As of last July, miners based in the U.S. accounted for 35.4% of the hashrate on the network.

Most cryptocurrencies declined on Friday as traders reacted to geopolitical risks emanating from Russia and Ukraine.

On Friday, U.S. President Biden urged Americans to leave Ukraine immediately, warning “an invasion could begin at any time.” For now, the U.S. has ruled out sending troops into Ukraine despite Russia’s military activities.

Bitcoin (BTC) dropped as much as 5% over the past 24 hours, compared with a 4% decline in ETH and a 7% dip in SOL. Stocks were also lower while traditional safe havens such as gold and the U.S. dollar rose. Markets eventually stabilized later in the New York trading day.

Technical indicators are mostly neutral for bitcoin, showing support at $35,000-$40,000 and resistance at $46,000.

Over the past 10 days, a majority of trading volume occurred at $41K-$41.5K BTC, according to Jason Pagoulatos, an analyst at Delphi Digital, a crypto research firm. “If that level is lost, we likely move towards the volume gaps left behind, which happens to coincide with $38.5K.”

Latest prices

●Bitcoin (BTC): $42334, −4.23%

●Ether (ETH): $2914, −6.53%

●S&P 500 daily close: $4418, −1.90%

●Gold: $1865 per troy ounce, +1.55%

●Ten-year Treasury yield daily close: 1.96%

Bitcoin, ether and gold prices are taken at approximately 4pm New York time. Bitcoin is the CoinDesk Bitcoin Price Index (XBX); Ether is the CoinDesk Ether Price Index (ETX); Gold is the COMEX spot price. Information about CoinDesk Indices can be found at coindesk.com/indices.

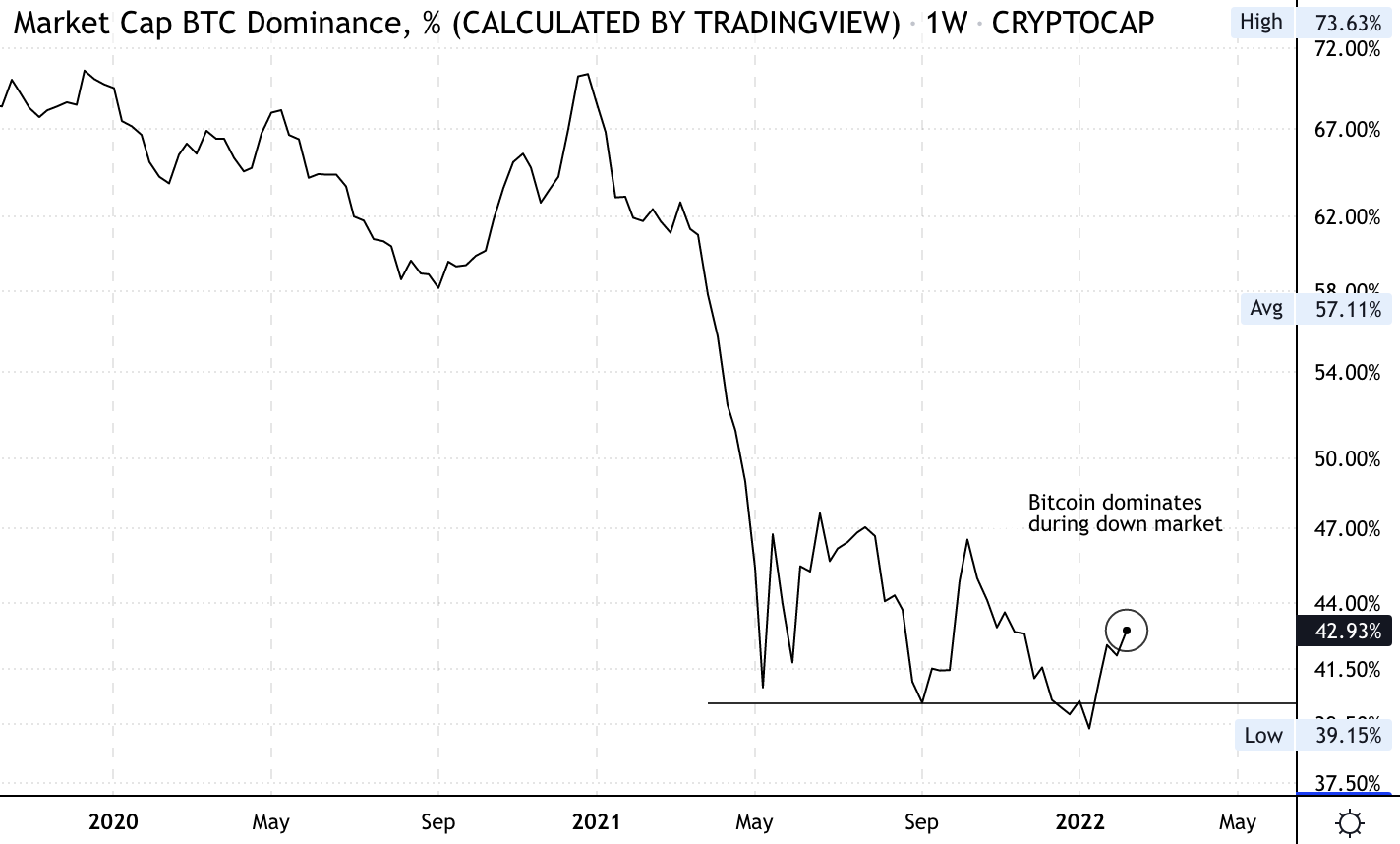

Bitcoin dominance rises

Bitcoin’s market capitalization relative to the overall crypto market cap rose above 40% this week. Typically, traders overweight bitcoin during market downturns because of its lower risk profile relative to alternative cryptocurrencies (altcoins).

During the 2018 crypto bear market, the BTC dominance ratio rose from a low of 35% to a high of 72%. And over the past year, the ratio declined by 30 percentage points as altcoins rallied ahead of bitcoin.

Some analysts expect bitcoin to remain under pressure for a few more months. “In last spring’s drawdown, it took about six months for bitcoin to recover,” NYDIG, a bitcoin holding company, wrote in a newsletter this week. “A similar timeline in the current drawdown would put a recovery date sometime in May.”

The bitcoin dominance ratio (CoinDesk, TradingView)

Altcoin roundup

Polkadot incentives: Astar Network, a parachain or parallel chain of the Polkadot network, has announced the $100 million Astar Boost Program fund to provide liquidity and offer financial support and incentive programs to smart contract developers. The company told CoinDesk that the program was funded through $22 million in fundraising, as well as an allocation of the native ASTR token.

Tether blacklists Ethereum address linked to Multichain hack: The address traces back to hackers who stole $3 million in cryptocurrency on the cross-chain bridge Multichain nearly a month ago, according to Etherscan’s labeling of transactions involving the wallet as well as a CoinDesk analysis. Whoever controls the address won’t be able to move funds so long as they are frozen.

NFT-linked house sells for $650K: Real estate startup Propy has sold its first NFT-backed property in the U.S., the company announced Friday. The 2,164-square-foot house in Gulfport, Fla., fetched $653,000 (210 ETH) at auction, with the winning bidder being awarded a non-fungible token as proof of the home’s ownership.

The governor of Hungary’s central bank has called for a European Union ban on cryptocurrency trading and mining. “It is undeniable that cryptocurrencies could be used to facilitate illegal activities and contribute to the formation of financial pyramids,” he said.

The Hungarian National Bank, the central bank of Hungary, published a statement Friday from György Matolcsy, the governor of the central bank, declaring that the “Time has come to ban crypto trading and mining in the EU.”

He noted that “China declared all cryptocurrency activities illegal last September” and Russia’s central bank has proposed “a ban on crypto trading and mining.”

Commenting on the Russian central bank’s crypto ban proposal, Governor Matolcsy said:

I perfectly agree with the proposal and also support the senior EU financial regulator’s point that the EU should ban the mining method used to produce new bitcoin.

In January, the vice-chairman of the Board of Supervisors of the European Securities and Markets Authority (ESMA), Erik Thedéen, called for an EU-wide ban on cryptocurrency mining based on the proof-of-work concept.

The governor of the Hungarian National Bank added that the Russian central bank “is right” in saying that “The breakneck growth and market value of cryptocurrencies are defined primarily by speculative demand for future growth, which creates bubbles.”

He emphasized: “The EU should act together in order to preempt the building up of new financial pyramids and financial bubbles. EU citizens and companies would be allowed to own cryptocurrencies abroad and regulators will track their holdings.” Governor Matolcsy further opined:

It is clear-cut that cryptocurrencies could service illegal activities and tend to build up financial pyramids.

Russia’s central bank proposed in January to outlaw all cryptocurrency operations in the country. “Cryptocurrencies also have aspects of financial pyramids, because their price growth is largely supported by demand from new entrants to the market,” according to the report published by the Bank of Russia.

However, the crypto ban proposal by the central bank was met with opposition as the Russian government, parliament, and even law enforcement departments are reportedly not willing to back the proposal.

Russian President Vladimir Putin subsequently urged the government and the central bank to reach a consensus on cryptocurrency, highlighting the potential of cryptocurrency mining in Russia. Last week, the Russian government approved a plan to regulate cryptocurrency.

Cryptocurrencies, according to Wells Fargo, are viable investments that have reached the “hyper-adoption” stage. The firm’s global investment team explained, “Cryptocurrencies have been following an adoption pattern similar to other new advanced technologies, such as the internet.”

Wells Fargo’s investment institute published a special report titled “Understanding Cryptocurrency” this week. The report attempts to answer whether it is “too early or too late” to invest in cryptocurrencies.

The Wells Fargo team explained:

We believe that cryptocurrencies are viable investments today, even though they remain in the early stages of their investment evolution.

They added: “We recommend professionally managed private placements for now, as the investment landscape is still maturing.”

The research team continued: “We see cryptocurrencies in the ‘early, but not too early’ investment stage, which is why we have emphasized investor education. The thrust of our view comes from global cryptocurrency adoption rates, which have quickly accelerated from a low base.” They noted:

Cryptocurrencies have been following an adoption pattern similar to other new advanced technologies, such as the internet.

The Wells Fargo analysts reiterated, “For today’s investor trying to figure out if we are early or late to cryptocurrency investing, looking at technology investing in the mid-to-late 1990s seems reasonable.” They added:

At that time, the internet hit a hyper-adoption phase and never looked back. Cryptocurrencies appear to be at a similar stage today … We are hopeful that greater regulatory clarity in 2022 brings higher quality investment options.

Nonetheless, the firm recommended: “Cryptocurrency investment options today, however, are still maturing and we advise patience. For now, we suggest the consideration of only professionally managed private placements.”

Wells Fargo started offering crypto investments to clients in August last year. The firm has also filed for a bitcoin fund with the U.S. Securities and Exchange Commission (SEC).

The price of Ethereum is expected to reach $6,500 by the end of the year, according to a panel of fintech experts. By 2025, it will have risen to $10,810, before nearly doubling to $26,338 by 2030.

Price comparison portal Finder updated its price predictions for ether (ETH) Tuesday. The company detailed:

Ethereum (ETH) will jump to US$6,500 by the end of 2022, according to Finder.com’s panel of fintech specialists.

In addition, “Ethereum is expected to hit $10,810 by 2025 before more than doubling to $26,338 by 2030, according to the average of the panel’s forecasts.”

The company explained that the panel of 33 fintech specialists was surveyed from Jan. 6 to Jan. 17 this year, adding that of the 33-panel members, 26 gave their ETH price predictions.

The fintech specialists are more bearish in their ETH price predictions than they were in October last year.

At that time, the panel predicted that the price of ether would hit $5,144 per coin at the end of 2021. It would then rise to $15,364 by the end of 2025 and $50,788 by 2030.

Commenting on the differences in price predictions this year and October last year, Finder wrote:

The panel’s prediction of the value ethereum may reach by 2030 has been dialed back significantly. The positive outlook for price growth in the cryptocurrency market was heavily affected by increasingly tightening international regulations and tumbling current values in early 2022.

At the time of writing, the price of ether is $3,182, based on data from Bitcoin.com Markets. ETH is up 18.3% over the past seven days and 3.1% over the last 30 days.

Finder added:

Sentiment from the panel towards ETH is strong, with over 80% having neutral to positive outlooks for its future. Over half (52%) of the panel think now is the time to buy ETH, with 30% saying you should hold onto what you’ve got. Just 19% say it’s a good time to get out.

According to a new report from KPMG, one of the Big Four accounting firms, investment in the crypto and blockchain space increased 5.5 times from the previous year to more than $30 billion in 2021. According to KPMG, 2021 will be a “blockbuster year for crypto and blockchain.”

KPMG published a report Monday on investments in the cryptocurrency, blockchain, and fintech space.

Noting that global fintech reached $210 billion last year, the Big Four accounting firm wrote: “We saw growing deal sizes in a wide variety of fintech subsectors — from crypto and blockchain to wealth tech and cybersecurity.”

Describing 2021 as a “Blockbuster year for crypto and blockchain,” KPMG detailed:

Investment in the crypto and blockchain space soared in 2021, rising from $5.4 billion in 2020 to over $30 billion.

“Globally, there was an incredible increase in the level of recognition for the potential role of crypto and its underlying technologies in modern financial systems,” KPMG noted.

“Increasing activity in the space has also sparked further action from central banks, some of which are considering the development of digital currencies in the footsteps of the digital yuan in China,” the global professional services firm further stated.

The KPMG report also highlights that global VC investment reached a record $115 billion in 2021, surpassing the previous high of $53.2 billion set in 2018.

Meanwhile, KPMG is investing in cryptocurrency. On Monday, KPMG in Canada announced that it has invested in bitcoin and ether, putting the cryptocurrencies in its corporate Treasury. “This investment reflects our belief that institutional adoption of crypto assets and blockchain technology will continue to grow and become a regular part of the asset mix,” said the Big Four accounting firm.

")