India carried out a massive demonetisation exercise that began on November 8, 2016. We covered the story of demonetisation extensively after it happened and had predicted that the program would be “All Pain, No Gain.” The release of the annual report of the Reserve Bank of India lays to rest all speculation on the matter.

According to the Indian newspaper The Hindustan Times, 98.6 per cent of scrapped notes have been returned to the Reserve Bank. This figure indicates that demonetisation was a failure, since the program had been designed to strand so-called ‘black money’ outside the traditional banking system. The return of such a high percentage of notes indicates that drug dealers, tax evaders, and others targeted by the program have managed to keep their ill-gotten gains.

The Hindustan Times reported in November 2016 that the Indian government had filed an affidavit before the Indian Supreme Court that stated:

“It will eliminate black money which casts long shadow of the parallel economy on our real economy. The poor and middle class, who are worst sufferers due to black money, will be benefited. It will reduce tax avoidance and bring more transactions into the formal economy.”

Brand Modi overcame demonetisation criticism

Demonetisation was intended to inflict short-term pain on the Indian people, but deliver long-term benefits by curbing terrorist finances, purging counterfeit currency and more. The government promised the people the moon and in return delivered them a damp squib that was poorly implemented and led to the death of at least 100 Indians.

The Indian people were largely supportive of the government’s plan because they believed in Prime Minister Modi. India’s leader kicked off the demonetisation process by painting himself as a crusader against black money. Modi had addressed a crowd in the tropical Indian state of Goa, saying:

“They think they can stop Modi by creating hurdles and harrowing him. I will not be cowed down. I will not stop doing these things, even if someone were to set me on fire alive.”

If you score a self goal, just move the goal post

The government is already in damage control mode after the Reserve Bank report was released, with finance minister Jaitley taking centre stage. According to Firstpost, direct tax collection was higher by 19 per cent during April-July compared with a year earlier. The government also is taking the defence that nearly 300,000 companies were ‘under scanner’ and 37,000 shell companies were discovered hiding black money.

The Finance Minister was seen shifting the goal posts of demonetisation with the Economic Times quoting him as saying:

“The real objects of demonetisation were formalisation (of the economy), attack on black money, less-cash economy, bigger tax base, digitisation, a blow to terrorism. We do believe that in each of these areas the effect of demonetisation has been extremely positive.”

The cost of demonetisation

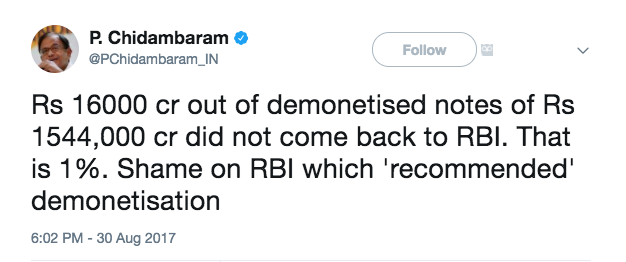

On the other hand, former Finance Minister P. Chidambaram was severely critical of the government. In a series of tweets, the man who has been India’s finance minister four times said:

Chidambaram also tweeted sarcastically saying, “RBI ‘gained’ Rs 16000 crore, but ‘lost’ Rs 21000 crore in printing new notes! The economists deserve Nobel Prize.” A crore equals 10 million.

India’s growth dented by its own government

Alarmingly, India’s GDP growth in Q1 2017 slowed to a trickle at 5.7 percent. This is the lowest figure in three years. The opposition Congress party used terms like “misery’ and described demonetisation as a “body blow” according to the Financial Express. The Hindustan Times reports:

“The economy lost steam primarily because of a sharp fall in mining, manufacturing and construction sectors, where demand remained muted even nine months after the government decided to scrap about 86% of cash in circulation to fight corruption and counterfeiting.”

Bitcoin is the real winner of India’s demonetisation

India’s demonetisation experiment was a clear failure, demonstrating that governments cannot always be trusted to manage monetary issues well. In fact, history is littered with examples where governments that have destroyed their own economies due to mismanagement. Zimbabwe, Argentina, Venezuela, Germany are all alarming stories of how bad people at the helm can destroy the lives of common citizens.

We are glad that we live in an era where there are alternatives to these government currencies, these alternatives are decentralised, digitised and available for everyone to use around the world. Bitcoin and other cryptocurrencies offer a hope to people when times are bad. India’s demonetisation pushed up Bitcoin prices and encouraged adoption in India. This is the silver lining of this story.

Leave a Reply

You must be logged in to post a comment.